Multiple EMIs? Here’s How It Affects Your Home Loan Eligibility

-

March 20, 2026 1:25 AM PDT

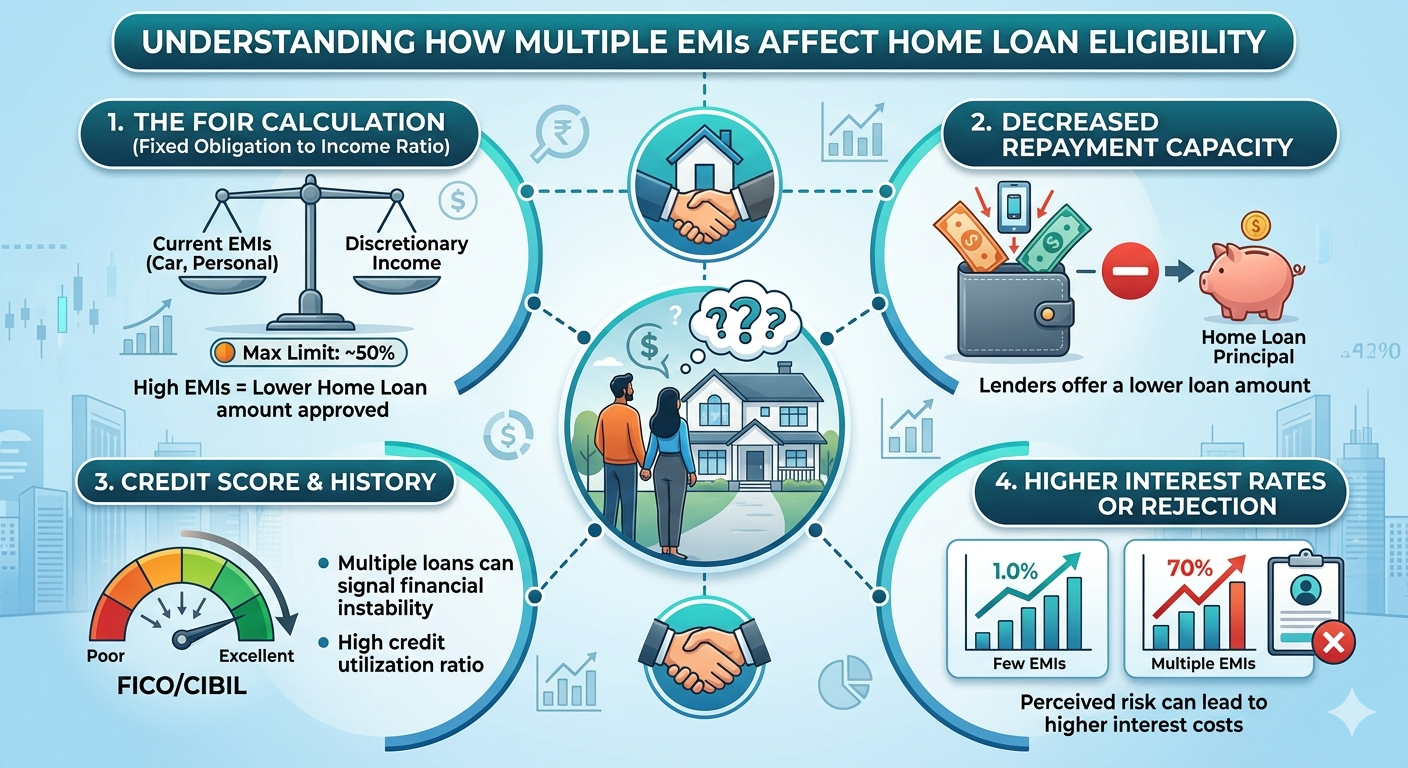

Why Existing EMIs Matter for Home Loan Eligibility

When you apply for a home loan, lenders carefully evaluate your repayment capacity. If you already have multiple EMIs—such as personal loans, car loans, or credit card dues—it directly impacts your ability to take on additional debt.

Banks and NBFCs use a key metric called the Fixed Obligation to Income Ratio (FOIR). This ratio determines how much of your monthly income is already committed to EMIs. Generally, lenders prefer your total EMIs (including the new home loan) to stay within 40% to 60% of your monthly income.

For example, if your monthly income is ₹50,000 and you’re already paying ₹20,000 in EMIs, your chances of getting a large home loan may reduce significantly. High existing obligations signal higher risk, which may lead to lower loan eligibility or even rejection.

How Lenders Calculate Eligible Home Loan Amount: Step-by-Step

Understanding how lenders calculate your loan eligibility can help you plan better:

Step 1: Assess Monthly Income

Your net monthly income (after taxes) is considered. This includes salary, business income, rental income, or other stable earnings.

Step 2: Calculate Existing EMIs

All ongoing obligations are added—personal loans, credit cards (minimum due), car loans, etc.

Step 3: Apply FOIR Limit

Lenders apply a FOIR cap (typically 50%).

Step 4: Determine Available EMI Capacity

Available EMI = FOIR limit – Existing EMIs

Step 5: Convert EMI to Loan Amount

Based on interest rate and tenure, the eligible EMI is converted into a loan amount.

Example:

· EMI = ₹20,000

· Interest Rate = 8% yearly → r = 0.08 / 12 = 0.00667

· Tenure = 20 years → n = 240

This EMI determines how much home loan you can get.

How Different Types of EMIs Impact Eligibility

Not all EMIs are treated equally. The type of loan you have can influence your eligibility:

1. Personal Loan EMIs

These are unsecured loans and carry a higher risk. Lenders view them negatively, which can significantly reduce your eligibility.

2. Credit Card Dues

Even if you pay only the minimum due, lenders consider it a liability. High credit utilisation can hurt both your eligibility and credit score.

3. Car Loan EMIs

These are secured loans, so their impact is moderate compared to personal loans.

4. Consumer Durable Loans (EMI on gadgets, appliances)

Though smaller, multiple such EMIs can add up and reduce your repayment capacity.

5. Education Loans

These are sometimes treated leniently, especially if repayment hasn’t started yet, but they still count as obligations.

How Different Lenders Treat Existing EMIs

Each lender has its own policies, but here’s a general idea:

Banks

· Strict FOIR limits

· Prefer stable income and low existing EMIs

· Better interest rates but tighter eligibility criteria

NBFCs (Non-Banking Financial Companies)

· More flexible with higher FOIR (sometimes up to 65%)

· Easier approval even with multiple EMIs

· Slightly higher interest rates

Fintech Lenders

· Faster approval process

· Use alternative data (like spending patterns)

· Suitable for borrowers with complex profiles

Choosing the right lender can make a big difference if you already have multiple EMIs.

Practical Ways to Improve Your Eligibility Quickly

If your eligibility is low due to multiple EMIs, don’t worry—there are ways to improve it:

1. Close Small Loans First

Pay off smaller EMIs like consumer loans or credit card dues to reduce your obligations quickly.

2. Increase Your Income Proof

Include bonuses, incentives, or additional income sources to boost your eligibility.

3. Opt for a Longer Tenure

A longer tenure reduces your monthly EMI, increasing eligibility (though total interest increases).

4. Add a Co-Applicant

Applying with a spouse or family member can significantly improve eligibility.

5. Maintain a High Credit Score

A score above 750 increases trust and may help you negotiate better terms.

6. Avoid New Loans Before Applying

Taking new loans just before applying for a home loan can reduce your chances of approval.

Documents & Proof Lenders Want When You Have Multiple EMIs

· When you already have ongoing loans, lenders may ask for additional documentation:

· Income Proof: Salary slips (last 3–6 months), bank statements, ITR for self-employed

· Existing Loan Statements: Details of all active EMIs

· Credit Report: To verify repayment history and liabilities

· Employment Proof: Offer letter, ID card, or business registration

· Bank Statements: To track your cash flow and spending habits

Providing complete and accurate documentation improves your credibility and expedites the approval process.

Conclusion

Having multiple EMIs doesn’t mean you can’t get a home loan—but it does make the process more challenging. Lenders focus heavily on your repayment capacity, and existing obligations play a major role in determining your eligibility.

By understanding how eligibility is calculated, managing your current EMIs wisely, and taking steps to improve your financial profile, you can still secure a Instant Home Loan Approval with favorable terms. Smart planning today can bring you one step closer to owning your dream home.

Disclaimer:

The information provided in this article is for general informational and educational purposes only. It does not constitute financial, legal, or professional advice. Home loan eligibility, interest rates, and lending criteria may vary depending on the bank, NBFC, or financial institution, as well as individual financial profiles. Readers are advised to consult with a qualified financial advisor or directly with lenders before making any financial decisions. We do not guarantee loan approval, accuracy, or completeness of the information presented. Use this information at your own risk.